|

|

|

|

|

|

|

|

|

Westend61/iStockPhoto / Getty Images

|

|

|

|

|

Oh, hi again. Tax season is upon us and if reading that brought chills down your spine, you may be a procrastinator. You’re not alone. |

|

|

|

|

|

|

|

|

|

|

Tax season tends to bring a sense of dread for many Canadians. It’s one of those tasks that’s easy to push to the bottom of the to-do list, right up until the deadline is suddenly around the corner. |

|

|

|

|

And plenty of people do exactly that. A 2024 H&R Block survey found that nearly a quarter of Canadians hadn’t filed their taxes with less than a week to go before the deadline. (A quick reminder: this year’s deadline is April 30.) |

|

|

|

|

But avoiding procrastination comes with advantages. Getting your paperwork together ahead of time gives you more room to figure out which deductions and credits you might qualify for – whether that’s related to childcare, moving expenses, tuition or medical costs. It also gives you time to double-check your documents and avoid mistakes that could lead to reassessments later. |

|

|

|

|

Of course, knowing this doesn’t always make it easier to get started. So I’m curious: When do you usually file your taxes? Are you someone who gets it done as soon as the T4 arrives, or do you wait until the very last minute? |

|

|

|

|

Take this quick survey and let me know, we’ll share the results in next week’s newsletter. |

|

|

|

|

Subscribe to the Retire Rich newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for Retire Rich here. |

|

|

|

|

|

|

|

|

|

|

|

How’s retirement going so far? What’s good and bad about no longer having to work every day? What’s been surprising to you? The Globe wants to hear your stories about life in retirement for its Tales from the Golden Age series.

If you’re interested in being interviewed and agree to use your full name and have a photo taken, please e-mail us at: goldenageglobe@gmail.com. Please include a few details about how you saved and invested for retirement and what your life is like now. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

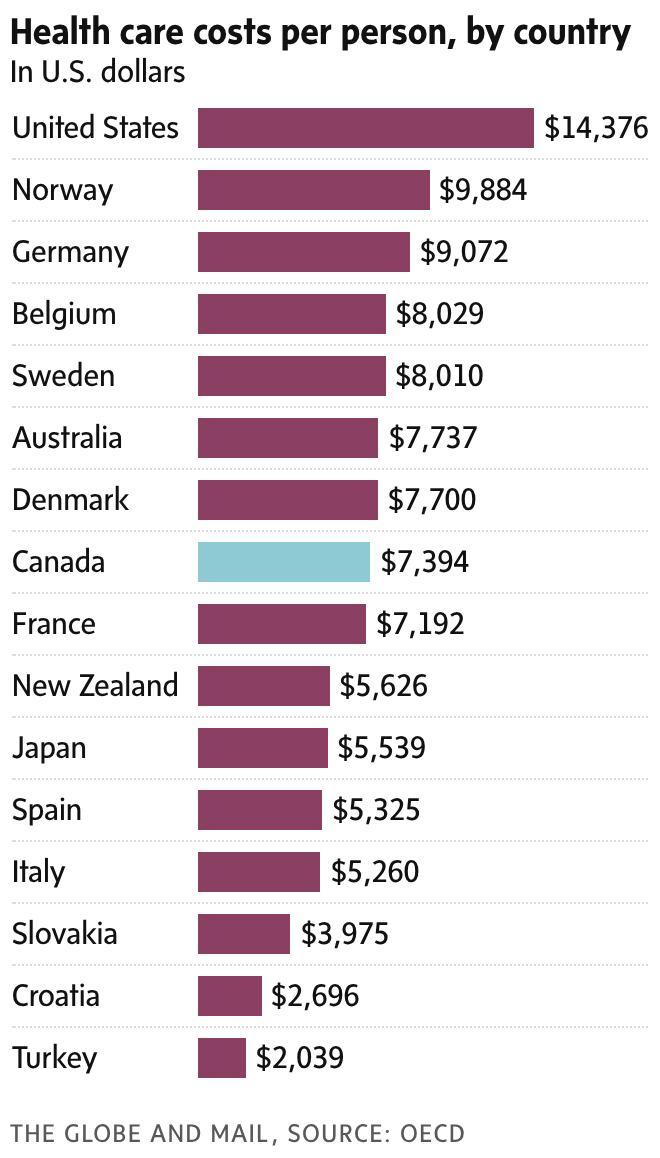

What’s happening: Canada spends a similar amount on health care compared with other developed countries, but the money isn’t being spent evenly across all areas. We have fewer machines, such as MRIs and CT scanners, than many peers, and a large share of spending goes toward end-of-life care and system costs like salaries. |

|

|

|

|

Why it matters: Where the money goes affects the care people get. Spending more at the end of life, and less on equipment and access, can mean longer wait times and fewer services. Yes, our population is rapidly aging,

but many European countries have older populations than Canada. These trade-offs could put more pressure on the system and on future retirees who will need to rely on it. |

|

|

|

|

Plus: If you’re looking for a laugh, check out this parody of the popular medical drama The Pitt from This Hour has 22 Minutes. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retirees Jeremiah, 66, and Kimmy, 63, have a house in Toronto valued at $2.2-million and $2.9-million in invested assets. EDUARDO LIMA/The Globe and Mail

|

|

|

|

|

|

|

|

|

|

|

The situation: Jeremiah, 66, and Kimmy, 63, are retired with two adult children, one of whom is in medical school. With a $2.2-million home and nearly $3-million in investments, they want to spend more in the early years of retirement, traveling with their kids and helping cover tuition, while they’re still healthy. |

|

|

|

|

The numbers: The couple plans to spend $183,000 a year after tax for the next few years, before gradually scaling back. They expect to spend about $30,000 annually on travel and $100,000 total to support their daughter’s education. Their total assets are about $5.3-million, and they are drawing roughly $15,400 a month from their retirement accounts. |

|

|

|

|

The advice from a financial planner: Their plan is achievable, and even conservative. Projections show they can meet their goals with a cushion, with enough left over to leave an estate. Still, the planner suggests diversifying beyond Canadian stocks, rethinking GIC-heavy holdings over time, and sticking to a gradual spending decline to avoid running short later in life. |

|

|

|

|

|

|

|

|

|

|

|

|