|

|

|

|

|

|

|

|

|

A row of new homes in Ottawa. Home insurance premiums in Ontario rose 45 per cent between 2019 and 2025. Sean Kilpatrick/The Canadian Press

|

|

|

|

|

Ontario home insurance premiums are climbing, but it’s not clear what Canadians are getting for the higher payments. |

|

|

|

|

Rates rose 6.2 per cent year-over-year in 2026 to an average of $2,235, driven by overwhelmed sewers, pumps or septic tanks, and wind and hail damage, according to a Rates.ca Home Insuramap report. |

|

|

|

|

Northern Ontario is home to all 10 of the province’s priciest towns, where premiums can soar to nearly 49-per-cent above the provincial average. |

|

|

|

|

If you happen to live in Cochrane Ont., your premiums may have gone up as much as 16 per cent to a whopping $3,322, while residents of Newmarket continue to see some of the lowest annual rates at $1,709. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Flood plain maps, which track areas at high risk of flooding, continue to shift, and insurers are not only raising premiums but also charging extra for coverage that used to be included in many policies. To make matters worse, tariffs and global conflicts are raising the cost of repairs. |

|

|

|

|

In fact, home insurance premiums spiked 45 per cent between 2019 and 2025, Statistics Canada data showed. |

|

|

|

|

|

|

|

|

|

|

“The cost of materials and labour is more expensive, there’s supply chain issues due to events overseas ... the physical materials are just more expensive today,” said Matt Hands, VP of insurance at Ratehub. |

|

|

|

|

But when it comes down to getting a payout, it’s rarely smooth sailing. |

|

|

|

|

After dipping 9 per cent between September, 2022, and the end of August, 2023, the number of complaints received by the Financial Services Regulatory Authority involving property insurance providers – including home insurance for tenants, homeowners and condo owners – rose 50 per cent between September, 2023, and August, 2024, and spiked 38 per cent between September, 2024, and the end of last August, according to data provided to The Globe. |

|

|

|

|

When the worst happens, many are caught off guard by what their insurance policy actually doesn’t cover. |

|

|

|

|

A burst pipe, for example, is often included in a standard policy, while overland flooding caused by heavy rain or snowmelt, is generally not – one of the “biggest misconceptions” that people have, according to Mr. Hands. |

|

|

|

|

At The Globe, I’ve often reported on the challenges homeowners face when filing insurance claims, ranging from difficulties getting reimbursed when they choose their own contractor instead of a preferred vendor to lengthy delays in completing cosmetic repairs and cleanup after emergency work. |

|

|

|

|

I want to hear about your experience with home insurance for an upcoming story. Tell me about it by taking our short poll. |

|

|

|

|

Subscribe to the On Money newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for On Money here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

One housing segment that’s doing quite all right: luxury Remax Canada’s 2026 Spring/Summer Spotlight on Luxury Report showed luxury housing sales spiking across a growing number of smaller and mid-sized Canadian markets, including Calgary, Edmonton, Saskatoon, Winnipeg and Ottawa. |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

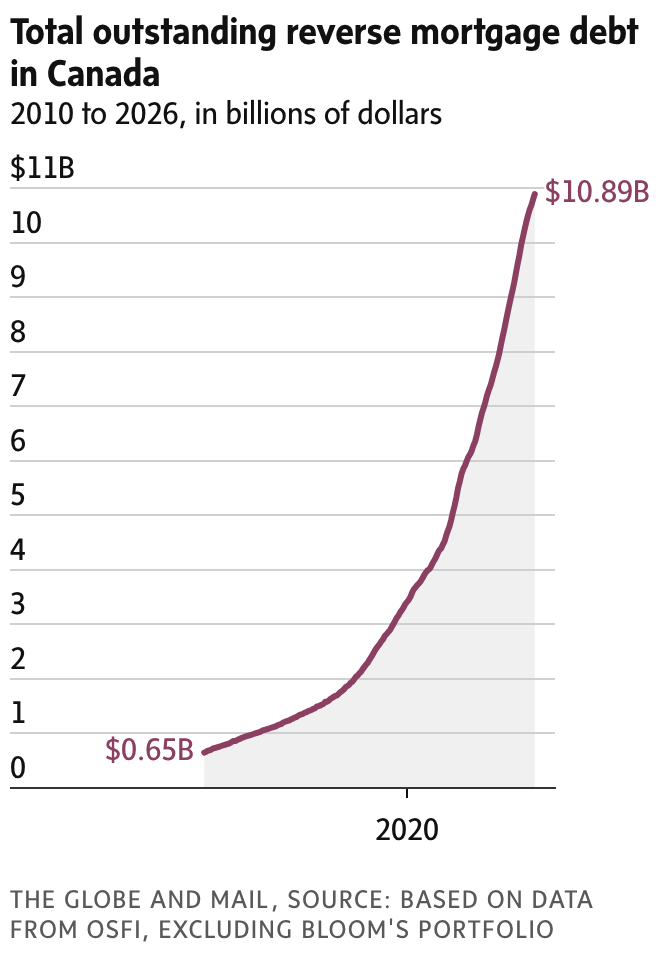

Hanif Bayat looks at Canada’s reverse mortgage market, which has quietly grown to almost $11-billion. |

|

|

|

|

|

|

Calling first-time buyers from the market peak

If you bought a condo in the last five years, journalist Kelsey Rolfe would like to speak with you. She’s working on a story for The Globe about how first-time buyers are doing now: Are you happy with your place? Have you tried to rent it out or sell it? If you’re open to an interview, e-mail her at kannerolfe@gmail.com. |

|

|

|

|

|